Welcome to our July 2025 Recap:

July Update of the Commodity and Economic Situation

As of the writing of this missive, we have a relatively big miss in Non Farm Payrolls and a hefty downward revision to prior numbers. This should not come as a surprise. While there may be laudable goals in the President’s agenda, forcing them all to fruition in six months is likely to break things. The economy, in our opinion, has never fully recovered from the COVID phenomenon. The massive shutdowns and disenfranchisement, coupled with the mass population movements, wanton government spending has created the dislocations we are dealing with. Trump has added wildly uncertain tariff regimes, attacks on drug companies, a potential set of aggressive sanctions aimed at countries which trade with Russia and a domestic base which is roiling over his failed promises. In the past, the US only dealt with one scandal at a time. The current situation is like condensing the entire Clinton presidency into six weeks. This can hardly be healthy considering the incredible reach of the modern bureaucratic state.

Not that we need to mention it, but the month was kind to Mr. Trump. He did negotiate a trade deal with the Europeans which saw them agreeing to purchase $750 Billion of natural gas, invest $600 Billion and otherwise remove tariff blocks on agriculture. The deal seems to be a lopsided victory for the US. There are also elements of mandated purchases of US defense hardware. The deal has many moving parts, but some of them are troublesome. First, as the Peterson Institute points out (https://www.piie.com/blogs/realtime-economics/2025/trumps-very-bad-trade-deal-europe), the average tariff of 15% on most goods is a significant increase. To the extent that Russian gas is globally marginalized, US energy prices will begin to reflect the European prevailing prices, net of transport. The US consumer will see electric and heating bills that skyrocket. The deal will favor energy exporters (and defense), but the US consumer may find life more expensive.

From the point of view of the Europeans, one wonders what they are thinking. Yes, 15% is better than 30% tariffs. However, they are being forced to eschew Russian gas, and at the same time, have a growing problem with Qatar over sustainability and environmental concerns. The Qataris are threatening to suspend gas shipments.In effect, the Europeans are replacing pipeline sources (Russian) and LNG from an aggressive competitor (Qatar), with LNG from Houston. It isn’t hard to see that when DC needs to call Brussels to heal, they need only point to this one linkage. Agriculture is a third rail in Europe. It does not seem to take much for French farmers to protest and throw tomatoes or fill city halls with manure. How will Europe force American produce down European throats? There is already tension between original EU states and the new, primarily Eastern European, members over this subject.

The other part of the deal which doesn’t make sense is the accounting. Typically, if country A runs a trade deficit with B, the current account is negative (in deficit) and the capital account is in surplus (B is investing in A). If the Europeans simultaneously close the deficit (or it goes to a US surplus) and they invest in the US, then the US exchange rate must skyrocket against the Euro. Moreover, the Europeans either must bankrupt themselves or find sources of capital. Nothing about this deal suggests durability. The Europeans have been given rat poison and are insisting it is TicTac breath mints.

The other trade deals “secured” are with Japan, Pakistan, Cambodia, Vietnam and so on. Considering that most of the trade deals in the past took years to negotiate, we wonder how many “devil’s in the details” realizations will come to the surface. It makes great sense for any given country to agree to anything and then chip away at the details, biding their time until this presidency ends. There is a tentative deal with China, but the secondary sanctions for purchasing Russian hydrocarbons may undo this. The Chinese are turning into immense spoilers in this situation. They see the writing on the wall. The US is not a safe place to park the immense current account surplus. The freezing of Russian assets proves that point. This creates double trouble for the US. First, without massive Chinese purchases of the US Federal debt, the Fed must monetize part of this debt or rates will meander further up. Second, the Chinese must do something with the dollars they accumulate. Gold would seem to be a natural and portable way to protect their surplus. We are headed back to the pre-Bretton Woods days of international payments.

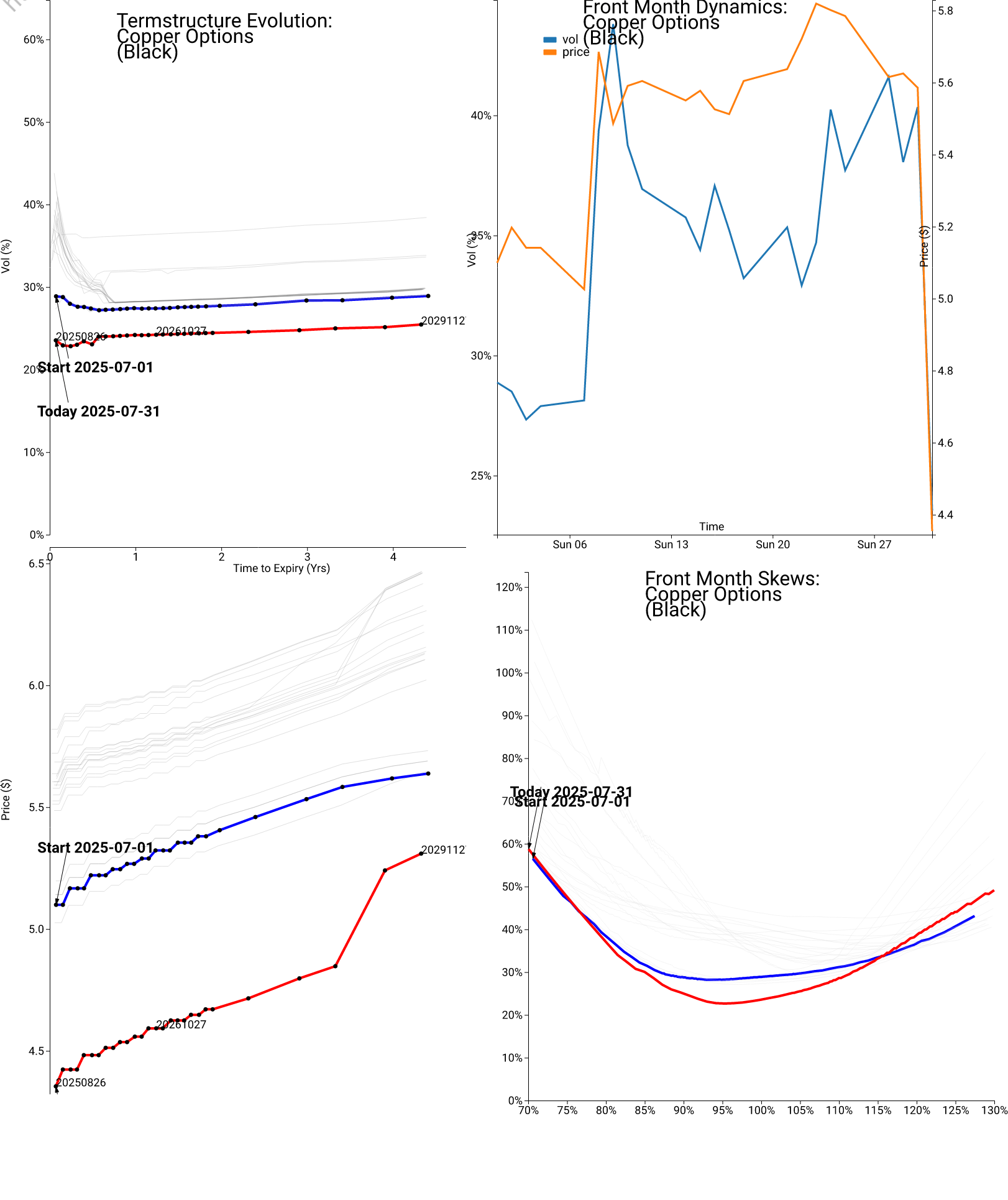

Here’s an example of the tariffs having a year’s worth of effect in a matter of days:

Copper imploded after the 50% tariffs were brought into existence. We are not sure about the wisdom of this move. The “Not In My Backyard” movement makes the opening of new mines unlikely. Crushing the price of copper in the US makes it economically infeasible to open new mines or revisit old mines. The largest producers of copper are Chile and Peru, neither of which would seem to be an American adversary. Destroying COMEX trading would also seem to run contrary to Making America Great Again.

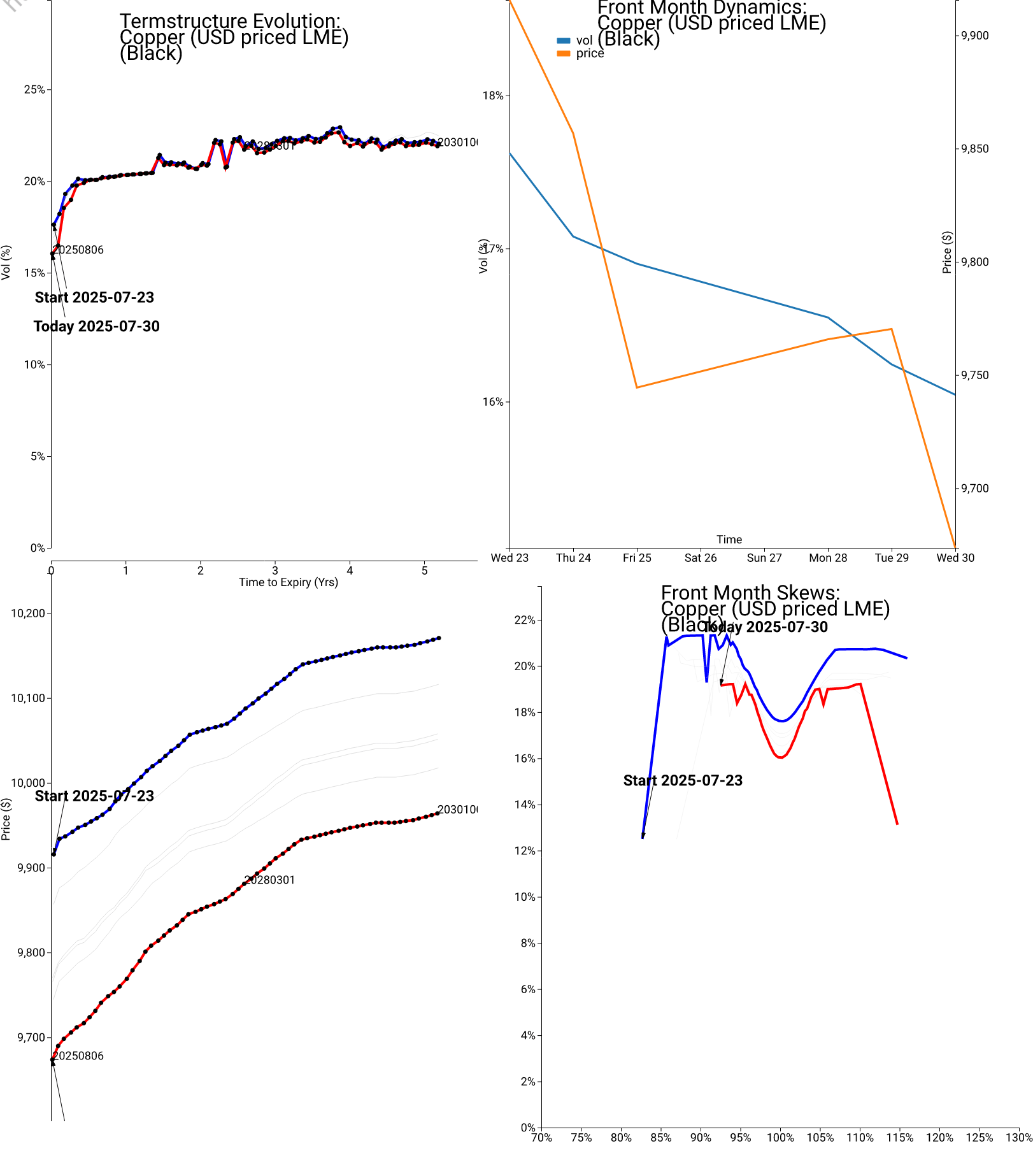

For comparison here is the LME contract

While LME may suffer from trust and opacity issues, it could be a competitor venue.There is also no reason why SHFE (Shanghai Futures Exchange) copper could not become the de facto world benchmark. Exchanges and the entire FIRE sector of the US economy has been the one place where the US has excelled. Moves like this put this sector at peril.

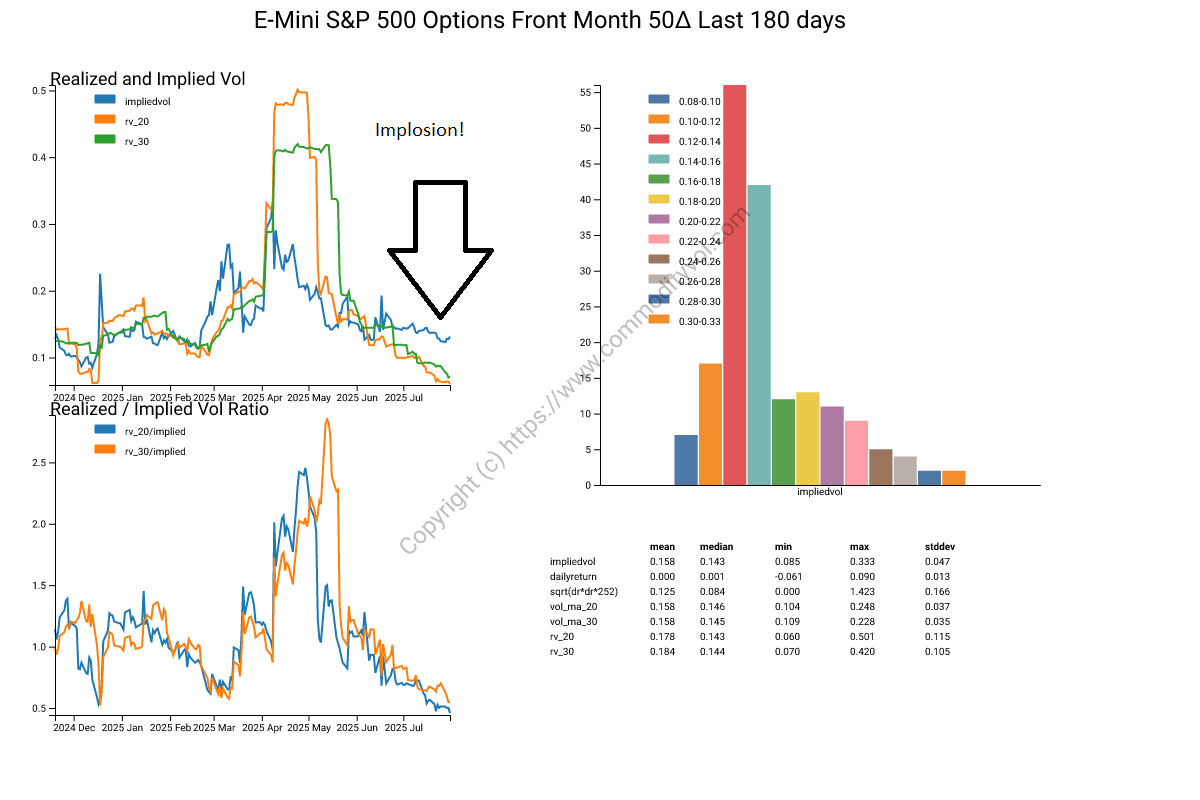

Equity markets are continuing in their alternate universe. Up until recently, the party line was that Americans were optimistic and that was the reason for the levitation. Here’s implied and realized vol for the E-Mini SP500 contract.

Both realized and implied vols are in the doldrums. It is hard to put all of this in perspective. We have trade fiascoes, wars and near wars, nuclear exchange threats and so on, yet there isn’t even a hint of risk in the air.

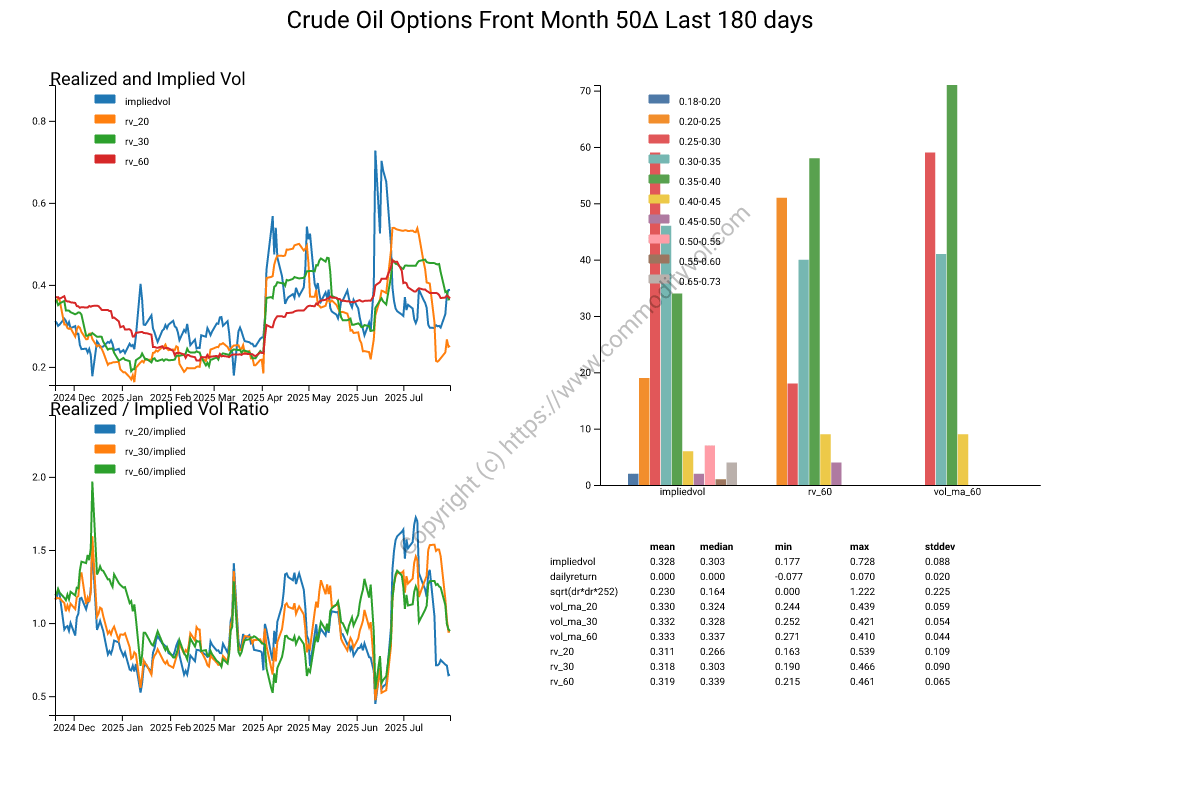

Additional sanctions on Russia seem to have brought some life to vol on oil

Though even there, the market acts as if a durable peace has materialized in the Middle East. With that, we turn to our roundup of the action this past month.

Forex

Futures fell for all of the traditional currencies. The dollar strength did not extend to crypto where both Ethereum and Bitcoin futures were up. Vol was crushed in everything except Ethereum futures.

Foreign Exchange ATMBitcoin DetailEthereum DetailYen DetailEuro DetailRates

Interest rate futures were down across the board, but this does not include August 1st. The administration's search for a quick fix is unlikely to do anything but ignite inflationary expectations. Obviously, the horrible non-farm payrolls number will put pressure on the Fed to cut rates, but, as we've stated before, the market determines rates. The double whammy of inflation running hot and fewer natural buyers of US bonds will put a damper on what can safely be accomplished. There is no way to go back to the Greenspan halcyon days. Vol was mostly down on the month.

Interest Rates ATM30 Year Detail10 Year DetailSOFR DetailEquity Indexes

July was another strong month for equity indexes. ES was up about 2% while the NASDAQ was up 3%. Vol was down dramatically in both, as well as the VIX. We showed that vol got aggressively dumped after the limited engagement in Iran. There is not one bit of forbearance in this market. Facing a slumping real estate sector, tariffs, uncertainty and wars it plods higher.

EquityIndex ATMSP500 DetailRussell DetailVIX DetailMetals

Metals are a mixed bag. Copper was absolutely destroyed. Gold was slightly down, although that changed on August 1st. Silver and palladium were strong, but platinum was offered. Vol was mostly offered with the exception of Tin and Palladium.

Metals ATMGold DetailPlatinumCopper DetailAgs

European Corn was up on the month and CBOT corn was down. Feeder and live cattle were up again. With vol in live cattle experiencing a lively bid. Beans and meal were down while bean oil was up. Both beans and meal exhibited sharply bid vol. Wheat was down on lower vol. Deals signed with Australia and Japan promise to send American beef to those countries, but as discussed, there might be a lot of reasons which will retard that flow.

Ags ATMFeeder Cattle DetailLive Cattle DetailCorn DetailSoybean DetailAgs DetailsEnergy

Renewed sanctions on the Russians coupled with secondary sanctions against India and China lit a fire under Brent and WTI. Vol was up smartly in both. There are rumors that if India defects the Russians and agrees not to purchase oil, then the Russians might retaliate by stopping the CPC pipeline which transports Kazakh oil across parts of Russia. Again, given the geopolitical tension all over the place, we are surprised that the moves have been so measured. Natural gas was down dramatically on lower vol. Apparently the European energy deal wasn't enough to overrule the weather in the US.

Energy ATMUS Natty Gas DetailWTI Crude DetailDetails EnergyAs always, we welcome you to visit our website and hope to help you manage risk!

CommodityVol.com is here to serve your needs around modeling, forecasting and understanding the market. If you have needs for commodity skews, parameterized surfaces (including stochastic volatility models), please do not hesitate to contact us! If you like any of the views we create, we are happy to deliver them to you. Contact Us